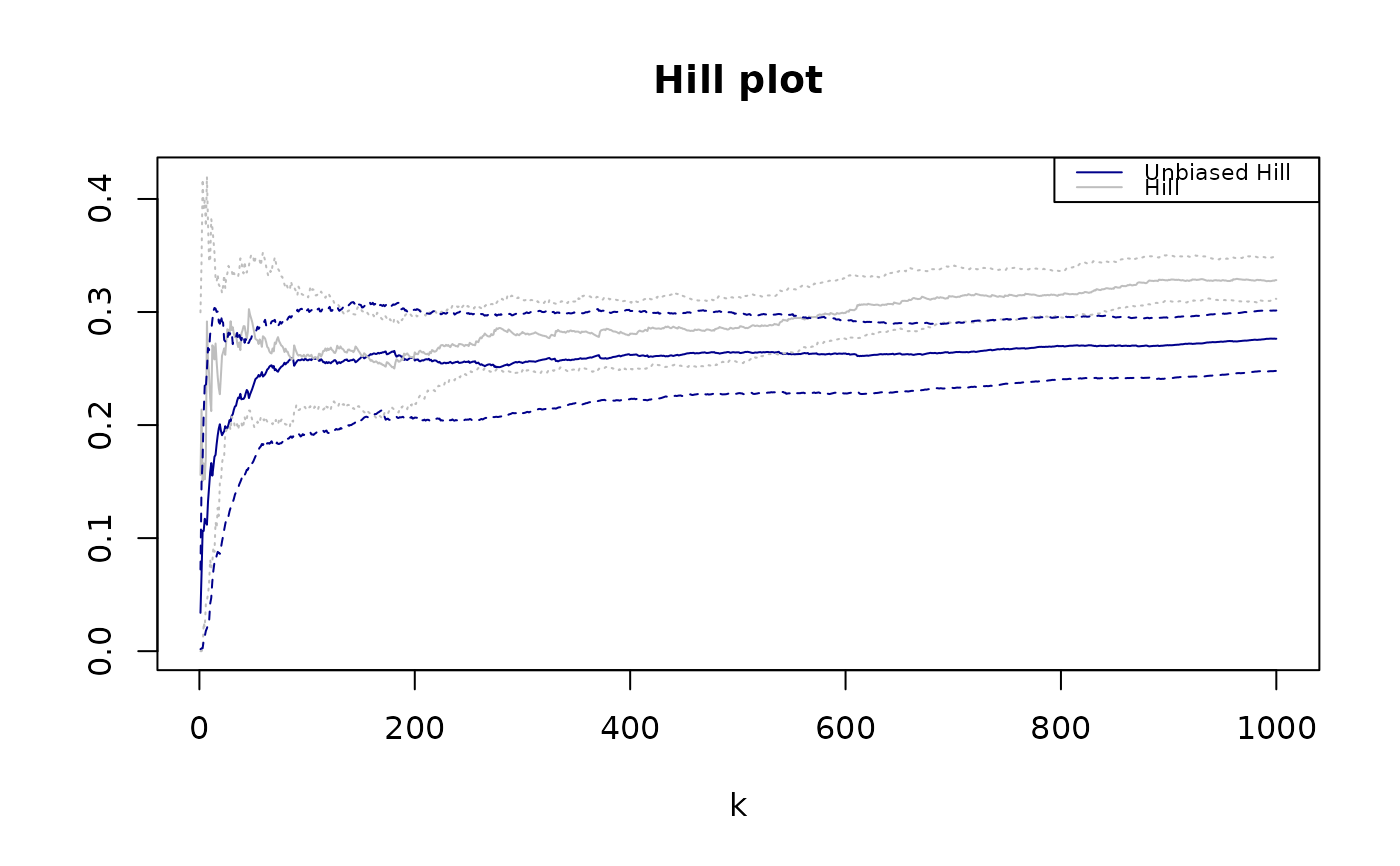

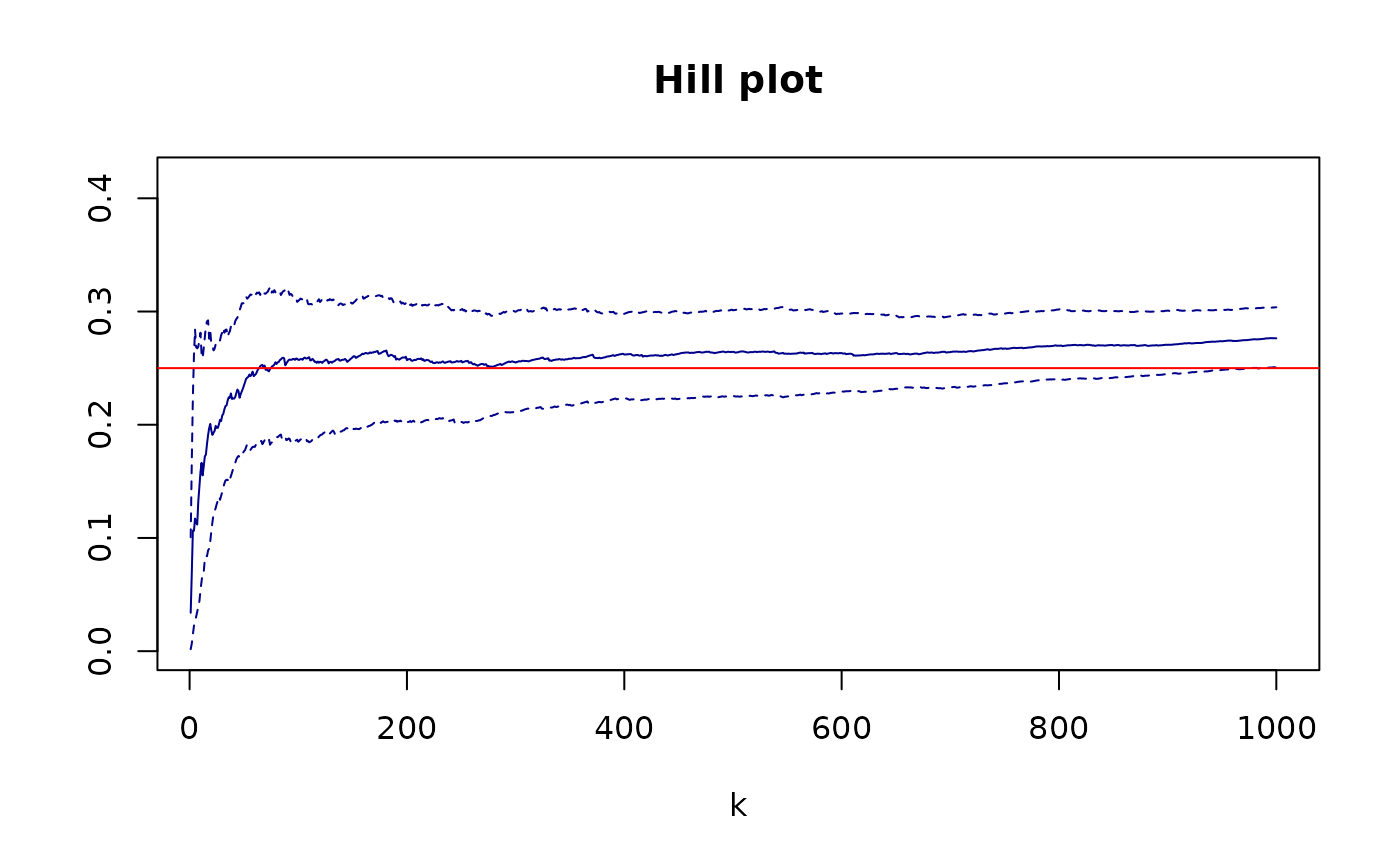

This function computes the (tail)-index as a function of k It returns the unbiased Hill estimator from de Haan et al. with tuning parameter rho = 2

Usage

alphaestimator(

sample,

k1 = floor(n^(0.7)),

plot = FALSE,

R0 = 100,

hill = FALSE,

ylim0 = NULL

)Arguments

- sample

(Vector of nonnegative univariate entries)

- k1

(Integer indicating the number of high order statistics to consider for inference)

- plot

(T or F indicate if the plot of Hill estimates as a function of k must be shown)

- R0

(Integer with the number of bootstrap replicates to consider for computing confidence intervals)

- hill

(T or F indicate if the classical Hill-plot is also plotted)

- ylim0

(Vector with lower and upper bounds of the y-axis for the plot )